Mar-a-Lago Accord: Bretton Woods in Reverse

Tariffs as threats. Bonds as blackmail. Gold as a gimmick. Welcome to America’s fiscal endgame—wrapped in an alliance treaty and sold as salvation.

“You want U.S. protection, trade access, security guarantees? Start buying duration.”

Not a movie line. Not even policy. Just power—disguised as doctrine.

Allegedly leaked from a Signal chat inside the next administration, this single line captures the soul of the Mar-a-Lago Accord: coercive diplomacy, dressed up as economic salvation.

This isn’t some backroom tariff tweak or policy memo buried in an appendix. The Mar-a-Lago Accord is shaping up to be the most aggressive attempt to reset the global financial order since Bretton Woods—minus the consensus, minus the credibility, and minus the safety net.

Wrapped in nationalist varnish and gilded in the aesthetics of power, the plan blends Plaza Accord nostalgia with a touch of fiscal brinkmanship and a whole lot of monetary coercion. It’s not a blueprint. It’s a loaded gun aimed at the foundations of the dollar system—and the rest of the world is expected to salute, pay up, and pretend it’s diplomacy.

From Plaza Accord to Palm Beach Power Play

The Mar-a-Lago Accord channels the spirit of the 1985 Plaza Accord—when the G5 collectively weakened the dollar to rebalance global trade. That was multilateral. That was diplomacy.

This time? It’s unilateral. It’s weaponized. It’s personal.

Tariffs aren’t a tool—they’re a threat. Security guarantees aren’t alliances—they’re invoices. Century bonds? IOUs stapled to the Stars and Stripes.

This isn’t Bretton Woods. It’s Bretton Brass Knuckles.

The architects of this new order—Stephen Miran and Scott Bessent—don’t see America’s chronic trade deficit as a bug. They call it a feature. In their telling, the U.S. must run deficits to meet global demand for dollar assets. Not poor fiscal discipline—global service provision.

It’s a seductive narrative. And a dangerous one.

“We’re not addicted to debt,” they argue.

“The world is.”

Break the Dollar to Fix the Trade Gap

Here’s the trade playbook they won’t say out loud:

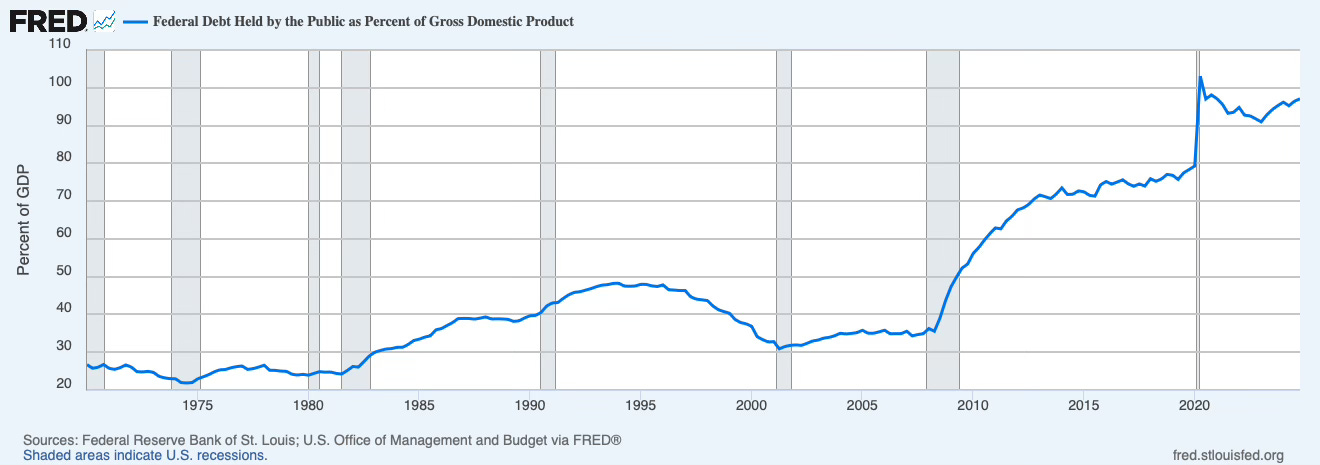

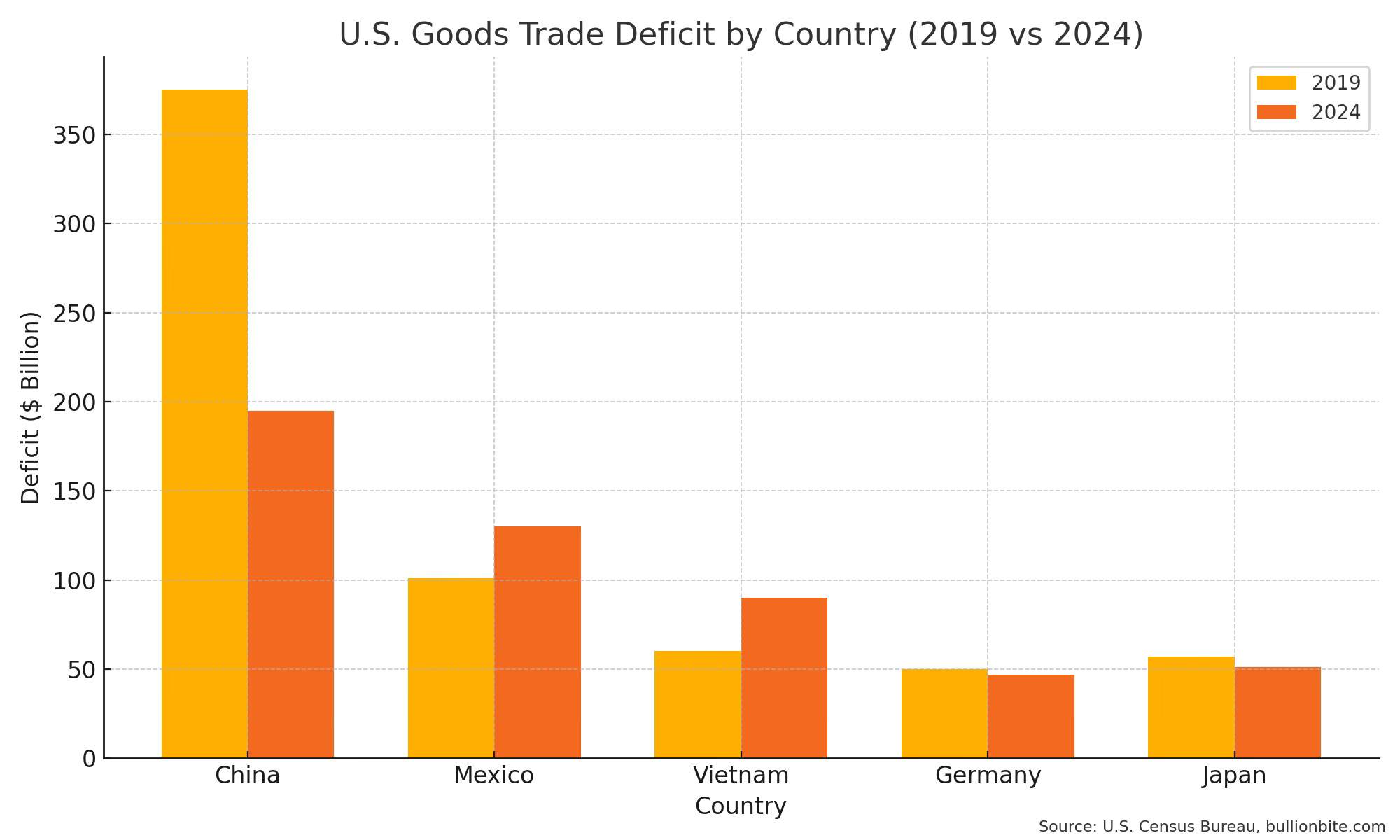

The U.S. trade deficit persists (~3% of GDP).

China’s share is falling—fast. From ~40% in 2019 to ~25% in 2024.

Mexico and Vietnam are stepping in.

And the bleeding’s in consumer goods: electronics, autos, pharma.

Enter tariffs.

Autos already face 25% duties. Pharma is next. Venezuelan oil? Stack the tariffs and you’re looking at 45%.

But here’s the catch:

Reshore too much, you kill the imports that fund tariffs.

Negotiate trade deals, and you have to lower tariffs—again, less revenue.

It’s circular logic with sharp elbows.

And all of it, supposedly, weakens the dollar — or burns it down trying.

Make Allies Pay—In Bonds

This is where the Accord stops pretending to be policy—and starts playing geopolitical hardball.

The proposal?

Force allies to hold non-marketable 100-year Treasury bonds—a.k.a. Century Bonds—as payment for U.S. security guarantees.

In Miran’s own words:

“If the U.S. restores freedom of navigation in the Red Sea at great cost, there must be further economic gain extracted in return.”

In plain English?

You want U.S. warships? Buy our bonds.

Japan is first in the crosshairs.

Yield Curve Control is unraveling. JGBs are under pressure. FX-hedged U.S. Treasuries are yield-positive again.

The Mar-a-Lago team sees a window:

Yields rise → Japanese insurers rotate into USTs → Washington delivers the ask: “Buy duration, get protection.”

A sovereign debt trap—wrapped in an alliance treaty.

Gold Games and the Great American Pawn Shop

The next phase isn’t policy—it’s balance sheet theater.

Step one:

Revalue U.S. gold reserves from $42.22/oz to ~$2,900/oz. Not out of honesty—just accounting sleight of hand.

Step two:

Book the difference as “equity.” Magically inject $800–900 billion without raising taxes or passing legislation.

Step three:

Create a Sovereign Wealth Fund—not from surplus, but from marked-up assets and creative math.

Let’s not kid ourselves.

This isn’t national strength. It’s a liquidation.

Parks, IP, land—anything public becomes collateral.

It’s not monetary strategy. It’s a pawn shop with a flag on the roof.

The goal? Inflate the asset column. Distract from the deficit crater.

And gold tricks? They’re just the opener.

From Gold Tricks to Default Theater

Repriced gold. Repackaged risk. And a Treasury market held hostage.

The real bomb is the so-called “User Fee” strategy.

Which is code for: selective default—wrapped in legalese.

Here’s the playbook:

Use IEEPA to withhold interest on Treasuries held by “hostile” nations.

Call it a “national security adjustment.”

Start small. Watch the market. Scale up if no one screams.

But the market always notices.

Because once credit risk enters the world’s benchmark “risk-free” asset, everything changes.

Treasuries aren’t just bonds—they’re the $25 trillion cornerstone of global finance.

Shake that, and everything priced off them starts shaking too.

Need an example?

Remember Liz Truss’s mini-budget?

Gilts exploded. Pensions buckled.

The Bank of England had to rescue itself.

Now replay that scene.

But swap in the U.S. Treasury market.

And globalize the fallout.

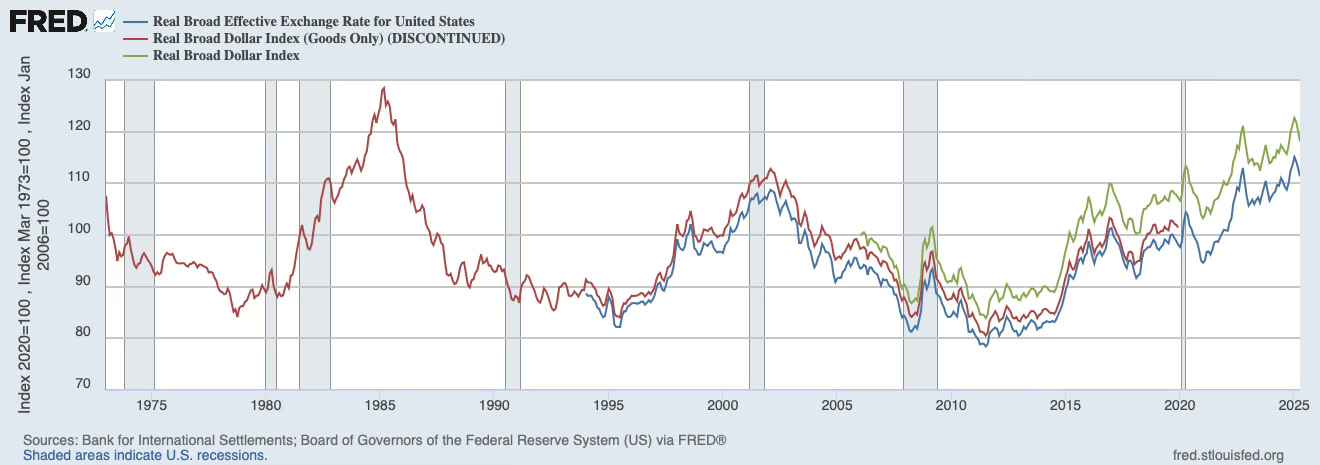

The Strong Dollar Isn’t the Problem

Team Trump wants you to believe the dollar is “too strong for its own good.”

But that’s not a bug—it’s a feature. And it didn’t happen by accident.

The dollar’s strength is rooted in U.S. fundamentals:

High productivity

Rule of law (mostly)

Technological edge

Deep, liquid capital markets that the world still trusts

Yes, America runs a structural trade deficit. But blaming that on a “too-strong dollar” is like blaming a Ferrari for speeding because it has a good engine.

The real culprit? A fiscal policy that’s been mainlining stimulus for decades without ever sobering up.

Reagan, Bush, Trump—it’s the same formula:

Tax cuts up front, deficits forever.

The 1980s, 2000s, and 2017 tax overhauls were never matched with spending discipline.

Then COVID hit—and fiscal restraint was left in a shallow grave.

So no, deficits aren’t the price of reserve currency status. They’re the price of political cowardice.

If America has to borrow trillions, it’s not because the world demands dollars—

It’s because Washington refuses to balance its own damn books.

When the World Stops Believing

So what happens if this Accord actually gets executed—even partially?

Dollar Detonation

The attempt to weaken the dollar “strategically” triggers something else entirely: capital flight.

Foreign holders demand compensation in the form of higher yields—or simply walk.

Treasuries aren’t dumped. They’re disowned.

Geopolitical Blowback

Allies stop pretending. NATO becomes transactional. Japan buys duration for protection, but Europe balks.

When security becomes a subscription model, don’t be surprised when clients cancel.

Market Repricing

Treasuries lose their mythological “risk-free” status. They start pricing like Argentine bonds with a better PR team.

Risk premia rise across the curve. Liquidity thins. Equities wobble. Margin calls whisper louder.

Gold Doesn’t Hedge—It Screams

The collapse of fiat trust doesn’t send investors to gold—it catapults them.

$2,900 is not a ceiling; it’s a signpost.

This isn’t a rotation. It’s a referendum.

Balkanized Finance

Dollar hegemony doesn’t die overnight. It bleeds out. Clearing becomes a weapon.

The world doesn’t abandon SWIFT. It simply builds around it.

The digital yuan gets a second look—and this time, not just from policy papers.

Controlled Demolition, Dressed as Policy

The Mar-a-Lago Accord isn’t a policy. It’s a fuse—lit quietly, burning through the foundations of global finance.

This isn’t about fixing trade. It’s about rigging the monetary scaffolding, then kicking it out from under the dollar—slowly, deliberately, and with plausible deniability.

Tariffs become threats. Bonds become weapons. Security guarantees come stapled to fine print.

It’s not diplomacy. It’s fiscal extortion in a tailored suit.

And the thing about leverage? It works—until it doesn’t. Because once you weaponize trust, you lose it.

This isn’t a rescue mission. It’s the controlled demolition of a system already cracking—

and we may not walk away from the rubble in one piece.