Debt Pause, Reality Resumes

Student loans were just the first crack. Now mortgages, credit cards, and middle-class credit scores are quietly caving in.

It took five years of borrowed time to arrive at this moment of reckoning. In Q1 2025, the student loan time bomb—carefully deferred through executive orders, pandemic panic, and legally shaky forgiveness schemes—finally detonated.

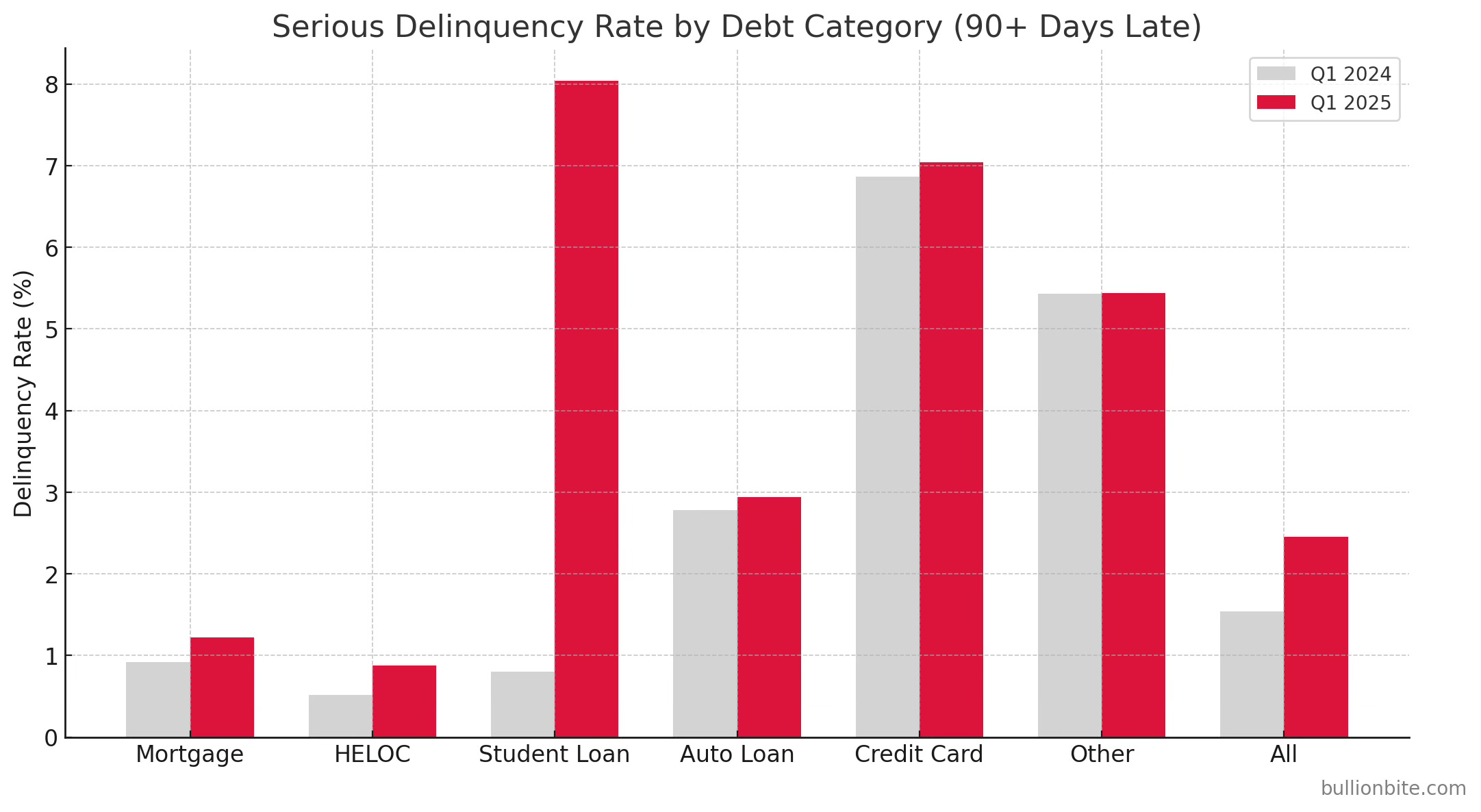

Delinquencies didn’t rise gradually. They exploded. From just 0.7% in Q4 2024 to over 8% in Q1 2025. That’s 5.6 million Americans officially behind on their loans. This isn’t a technical blip—this is a credit shock manufactured by policy… and it’s only just beginning to ripple outward.

The financial media shrugs. “It’s just 0.1% of GDP,” says Morgan Stanley. But anyone watching consumer health metrics knows better. This isn’t a rounding error. This is the ignition point.

For 43 months, payments were frozen. Then came a one-year “on-ramp” grace period shielding missed payments from credit reports. That ended in October 2024—and when it did, the dam broke.

These delinquents aren’t new. They’ve been in suspended animation, now resurrected by a system that sold them hope and delivered a trap. The New York Fed’s household debt report confirms it: over 2.2 million borrowers have seen their credit scores plunge more than 100 points. For those who were once considered prime borrowers, the average drop is a brutal 177 points.

We’re not watching people fall from grace—they were pushed.

Some economists argue student debt doesn’t matter because it’s unsecured. That logic is laughable.

A 650 credit score? No home loan.

A 590? Forget a 0% auto lease.

A 540? Good luck renting in half the cities in America.

Multiply that by 5.6 million.

That’s not just statistical noise—it’s an entire generation disqualified from financial adulthood.

Student loan delinquency isn’t about missed coffee runs. It’s about delayed marriages, postponed car purchases, crushed small business dreams. It’s about closing the gates to the middle class.

Morgan Stanley says the hit is $1–3 billion per month in lost consumption. Bloomberg thinks it’s closer to $63 billion a year. Either way, it’s real, measurable, and already unfolding.

The housing market feels it, quietly.

Student loan payments now average around $300 per month—comparable to a car loan. That pushes many borrowers beyond the debt-to-income threshold for mortgages. Every additional $1,000 in student loans reduces the odds of owning a home by 1.8%.

This isn’t just a statistic. It’s a blockade.

As credit scores tank, mortgage rates for subprime borrowers rise. Down payment requirements balloon. The dream of homeownership slips from reach. And who fills the void? Not first-time buyers—but BlackRock, Invitation Homes, and Wall Street.

The American starter home now belongs to asset managers.

This is no longer about just student loans.

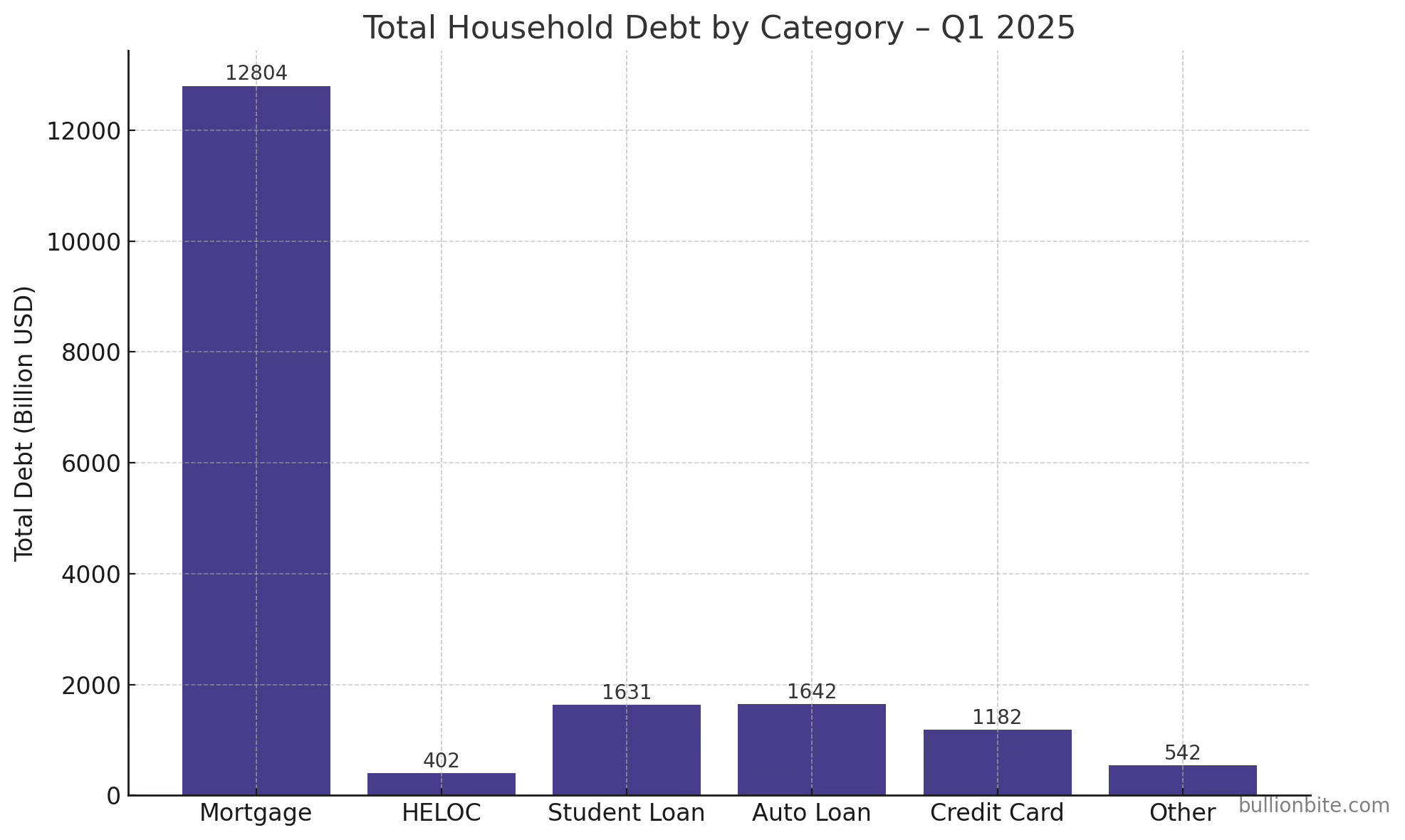

Delinquency is spreading. Mortgages, HELOCs, auto loans, credit cards—all flashing red. Credit card delinquencies have hit 7%. Total household debt? $18.2 trillion.

And all of this is happening before a recession or Fed hikes. The system isn’t crashing yet—but it’s suffocating. The bleeding is internal. Silent. Slow.

Student loans were just the first domino to fall. But they won’t be the last—and the rest aren’t standing nearly as firm as policymakers pretend.

Now comes the next phase: collections.

In May 2025, the Department of Education restarted default collections. That means wage garnishments, seized tax refunds, intercepted Social Security payments. Yes, even Social Security.

More than 11% of borrowers over 50 are 90+ days delinquent—the highest level in 20 years. In other words, we’re garnishing grandma’s Social Security to pay for a degree she co-signed 15 years ago.

You can’t parody this. But it’s real—because in 2005, Congress made student loans non-dischargeable in bankruptcy.

This is no longer just economic. It’s cultural.

A growing number of employers no longer see value in college grads. Surveys show that 8 out of 10 hiring managers report dissatisfaction: poor work ethic, phone addiction, unprofessionalism. These aren’t just skill gaps—they’re the byproducts of a credentialing bubble.

These aren’t gaps. They’re signals. Of a generation that paid premium prices for increasingly useless credentials.

Meanwhile, tuition rises. Administrative bloat expands. DEI departments metastasize. And the product? Increasingly irrelevant and unaffordable.

We are watching the collapse of the “college as golden ticket” myth in real time.

What’s next?

The SAVE Plan—the Biden administration’s flagship repayment model—is stuck in legal limbo. Lawsuits have frozen major components. Around 8 million borrowers are left in a kind of Schrödinger’s forbearance: not paying, but not moving toward forgiveness either.

If the courts reverse these programs, it could trigger retroactive balances, interest accumulation, and a second wave of defaults—just in time for the 2026 election cycle.

That would be a political nightmare. But it would also be a macroeconomic accelerant.

This isn’t just moral hazard. It’s macro hazard.

A $1.6 trillion portfolio with a 25% effective default rate isn’t a nuisance—it’s a systemic flaw. The U.S. economy won’t collapse tomorrow, but it’s already choking on decades of bad credit policy, overpromised returns, and educational ROI delusions.

We’re not headed for a sudden Lehman-style crash. We’re already in the slow-motion, Japanified version of collapse. It’s happening in real time.

The only question is whether policymakers will confront the truth—or reach for one more temporary fix. Another pause. Another promise.

History says: they’ll kick the can.

Markets say: someone’s going to trip over it.